In a 2006 survey, 30 percent of people without a high school degree said that playing the lottery was a wealth-building strategy.

Holy cow! That’s not a good sign. Of course if they spent a couple of minutes with the Incredibly Depressing Mega Millions Lottery Simulator they might be singing a different tune. If they took the money that they would have spent on lottery tickets and instead invested it in something like the stock market, they would end up with something more substantial.

Imagine again that you are age thirty and you plan to retire at age 65. If you save the $156 you spend on lotto tickets annually and place that money in an investment that tracks the S&P 500 index, which has produced an annual rate of return of 10.4% over the last 80 years, at the end of each year for 35 years, you will have approximately $46,000 at the end of that time period.

I’ve detailed how I organize my bank statements before. But sorting through a month’s worth of receipts at once has become a real burden. Back in December Woot.com, the one item a day shopping site, had a Woot-off where a succession of products are available for an undisclosed period of time. A Neat Receipts scanner came up and I took the bait. But it wasn’t until last week that I actually started using it.

And boy am I sorry that I didn’t start using this product earlier. It is a snap to scan a receipt, have the software read the contents of the receipt using OCR, and file them away in a database. In the box you get a USB-powered scanner, the software that does all the heavy lifting, a calibration card, a carrying case incase you take the scanner with you on the go, and a stand for propping the scanner up when you’re not using it (see below).

Setting up the scanner was a snap. First install the software and scanner driver then connect the scanner to your computer using the included USB cable. The first time you run the Neat Receipts software it will ask you to calibrate the scanner using the calibration card. Between when I opened the scanner box and the time I actually started using the Neat receipts system I had lost the calibration card. Luckily it’s not vital. You can print out your own replacement card using a standard inkjet printer. During first scan I put the receipt in face-up. When I saw the result, I was confused as it was completely white. It turns out you have to scan the receipt face down. The scanning processis really snappy as demonstrated in this video.

After you scan a receipt, the software will analyze the text and fill in the appropriate fields like vendor, date, sales tax, and price. The accuracy was pretty spot on. I only had to correct info for a few receipts. One problem I ran into is the software doesn’t share info from other receipts. For example you can enter address information from the receipt into the database. If you always shop at the same grocery store, NeatReceipts doesn’t automatically fill in this information from the first time you entered it. This seems like it would be a no-brainer to implement.

The software is clunky but fairly easy to learn. The main functions include viewing your scanned receipts, fields to enter information about the receipt, folders to categorize your receipt collection, and a search field for finding specific receipts.

The folder organizer works just like any file system: drag and drop. I don’t really understand why you might need more than 3 folders or so. One of the real advantages is the receipts are fully searchable. Any receipt can instantly be brought up with a simple search. This is the main advantage of the whole system.

If you need to export your receipts you have multiple formats. Any receipt, or group of receipts, can be exported as a PDF, Excel spreadsheet, or Quicken/QuickBook/ TurboTax file. I was hoping you could easily export all of your scanned receipt images to Quicken to embed with the appropriate transactions. Both programs know the date and how much the transaction was making it a snap to match up. But alas, exporting to Quicken only includes the financial information to enter as transactions. This is useless to me as my financial transactions are automatically downloaded from my bank over the Internet. Exporting the receipt info to Excel is easy with their spreadsheet mapping tool which lets you match which fields go to which columns in your spreadsheet.

It is important to backup your database with their backup tool which lets you save a single file to a safe location. One of the downsides of the Neat Receipts scanner is all of the information is stored in a proprietary .nr file. This means you will need to keep a copy of the software around if you ever want to view it later. This certainly isn’t a problem now, but 10 years down the line it might be.

So after getting everything up and running the Neat Receipts scanner has made my life much easier. Every night Instead of throwing my days receipts into an envelope I scan them into my computer. If I ever think I might need the phyical copy I’ll stash it away, otherwise my receipts end up in my trash can. After stapling my receipts to my bank statements for the past two years, I realized I’ve never needed to go back to one. This way I have everything saved and searchable in digital space rather than cluttering up physical space. Add the fact that I can pull up any receipt with a simple search query and I’ll never go back to organizing little papers by hand.

Buying an engagement ring for your significant other can be both exciting and nerve-wrecking at the same time. Thankfully I survived the process and can now offer these tips I picked up along the way.

Note: These tips are aimed at guys from the perspective of a guy.

Unless you’re the ballsy type, don’t try to pick out a ring on your own!

I thought picking out an engagement ring would be a straightforward task. But after seeing the thousands of different minute details to pick and choose from I quickly reconsidered. Just take a gander at BlueNile.com, a good starting point for ring shopping. Can you guess which diamond type your lover would like? White gold, yellow gold, or platinum? Solitaire, side-stone, or three-stone? Four-prong, six-prong, comfort fit, knife edge, intertwined, cathedral? These things matter.

Talk to your partner about the ring.

Keep in mind this ring will be with the two of you for the rest of your lives so the recipient better be happy with it. Besides, open communication is a good trait for marriage.

Set a budget before browsing

Engagement rings are the ultimate intersection between emotion and money. You run the risk of setting yourself up for disappointment if you dive in without setting any ground rules. It is easy to raise expectations when shopping around but damn near impossible to lower them. Coming to an understanding about budget and quality between the two of you beforehand will make things sail smoothly.

And it doesn’t make sense to go into debt before the wedding as there will be other things that require money after the two of you tie the knot (like a down payment on a house!). In other words don’t get more ring than you can afford.

Talk to other family members about your plans.

Not only does this fall under the category of the more communication the better, but you could also save a lot of money. You never know if a close relative has a diamond ring sitting in a security deposit box just collecting dust. Now you shouldn’t go around demanding old jewelry, but if your family doesn’t know that you are thinking about getting married they won’t know to offer their old gems.

The diamonds in Kristina’s ring were from my grandmother’s ring passed down to my mother. They were certainly better diamonds then I could afford and the sentimental value of the family history made the engagement ring unique and extra special i.e. more romantic.

If possible, record the proposal on video.

This is one of the biggest moments of your life. Capture it on video so you can show it to future generations and re-live the day in your later years. With the rise of online video, passing a video around to friends via social networks will bring you in contact with people you haven’t heard from in ages. People love seeing exactly how your proposal went down.

It all might seem daunting at first but take everything one step at a time. Try not to let the stress get to you while seeking out the perfect ring to satisfy the needs of both you. Keep your eye on the prize which should be to show your companion how much you care about them and that you want to be with them forever.

For more engagement ring shopping tips check out the guides at Mahalo.com and About.com

It has been nearly a month and I thought I would update everyone about the last Zune in the DC area. I managed to sell the digital media player on the Amazon Marketplace for $329.99, a 32% markup over the original price. I still needed an MP3 player for my daily commute and with the profit I decided to buy another Zune 80 online via Amazon.com instead of in person at Target. In this situation buying online was a much better deal for the following reasons:

Buying the player in person results in sales tax being tacked on. Here in Maryland, the sales tax is 5% so that would add an additional $12.50. Amazon.com doesn’t charge sales tax for Maryland residents.

Amazon.com offers a 30 day price match on it’s own products. If the price drops within 30 days of a purchase, Amazon will refund the difference. When I ordered the player on December 2nd, it was $249.00. Today it is being sold for $239.99, a difference of $9.00. Claiming a refund is easy. Just go to Amazon.com/refunds and send customer service an e-mail. If you don’t want to keep track of the price differences yourself, check out PriceProtectr.com which will send you an e-mail if there is any drop.

Both Amazon.com and any local store are sold out of the device, so I would have to wait either way. I don’t mind waiting which is why I decided to sell my first one when the demand was high.

Here is a final breakdown of the math:

1st Zune Bought at Target

$249.99

+$12.50 Sales Tax = $262.49 Total

Sold on Amazon.com Marketplace

$329.99 Price Sold

+$7.48 Shipping Credit from Amazon.com

– $10.35 Actual Shipping Cost (Added insurance to the cost)

-$28.14 Amazon Fee

– $262.49 Cost to Acquire = $36.49 Profit

2nd Zune Bought on Amazon.com

$248.99

+$5.58 Shipping and Handling

-$5.58 Free Super Saver Shipping

-$9.00 Price Difference Refund = $239.99

Final price for my Zune

$239.99 for 2nd Zune

-$36.49 Profit From 1st Zune = $203.50

Not bad for waiting a little bit longer and taking advantage of a unique situation.

A recent story appearing on CNN examines Britney’s spending habits revealed by court documents released November 1st. According to the papers Ms. Spears brings in $737,000 a month. Spears’ monthly expenses include $49,267 in mortgage for two houses, $16,000 for clothes and $102,000 on entertainment, gifts and vacation, according to her financial declaration.

Meanwhile, she spends zero on education, savings and investments and gives $500 a month in charitable contributions. With such an enormous income, if she saved just 1% a month she would have $88,440 at the end of a full year. This would be more than enough to ensure her children get through college. For the rest of her life she could take that $7,370 monthly contribution and dump it in an investment vehicle that returned 5% annually for a cool $8,387,324.38 by the time she turns 60. Of course what fun would that be? I guess we’ll keep seeing Britney albums and related schwag until she finally gets a clue or drives herself crazy into the ground. Hey, nobody said saving for retirement was glamorous.

Get Rich Slowly is holding a contest asking for people to submit their financial success stories. With this in mind, I began to reflect on where I am today in my experience with money.

I was raised to be financially responsible from a young age. When I was comfortable with the idea of an allowance somewhere near the first grade my Dad set up a personal Heimlich bank complete with my own custom printed checks. He wanted to instill the idea of writing out checks for things I wanted to buy as well as going over a monthly bank statement. I should clarify this wasn’t a real bank but rather an imaginary one between my parents, who would be the only people on the planet that would recognize my checks, and I. The habit has stuck with me as I now use the elaborate receipt filing system on my real bills that they taught me oh so long ago. It wasn’t until college when I realized how ahead of the game I was, personal finance wise.

Not only did I grow up ingrained with good money habits, but I was also genuinely interested in learning all that I could about finance issues. My friends in college certainly didn’t seem to think to much about their finances as my roommate used to throw away his bank statements without even opening the envelope and the people next door relied on unemployment benefits to help pay for their party habits. It was also a wake up call to see many people were paying for college by taking out student loans in their own names unlike my extremely fortunate situation of a full ride from Mom and Dad.

After college I was already ahead compared to my debt-laden classmates and I landed a good job with decent benefits. I knew I was in a special situation being 22 and debt free. I was anxious for my 6-month waiting period for my retirement benefits to kick in so I could contribute as much as I could into my 401(k). A couple of months ago I set up my 16% contribution with confidence that I was doing the right thing thanks to compounding interest and time being on my side. In August the company announced a Roth 401(k) option that would let my money grow tax free and because I had been reading up about these things previously, I immediately knew it was the perfect option for me to take advantage of.

In the end, my greatest personal finance success has to be the knowledge and wisdom I acquired early on to be able to capitalize on this once in a lifetime opportunity. Money can buy lots of things, but it certainly cannot buy more time.

Thank you Mom, Dad, J.D. at GetRichSlowly.org, and all of the personal finance sites out there sharing their wisdom.

Setting up an e-business is a heck of a lot easier than a traditional brick and mortar store. Customers are now accustomed to buying things online and the online world requires much less capital, and therefore much less risk, to get started. Online web magazine Vitamin had a feature story about following a small outdoor clothing startup as it tweaked it’s store front in hopes of converting more visitors into sales.

The beauty of online stores is they can offer a wide range of products that are easy to search for and compare. Offering as many options to sort through the potential offerings is just as vital as the amount of goods you have available. The online start up found it was imperative to offer navigation by brand as customers were drawn more to brand names than categories of goods. They also started out with a design that focused too much on up selling instead of displaying the available merchandise.

If you’re planning to set-up your own little online shop, this article will give you insight into some of the pitfalls that could arise while developing your online store front.

Staying on top of your finances takes organization. Credit cards, banks, retirement accounts, pretty much anything related to your money comes with a statement that you need to keep track of until your taxes are accounted for at the very least. Here is how I go about tackling this dreaded task.

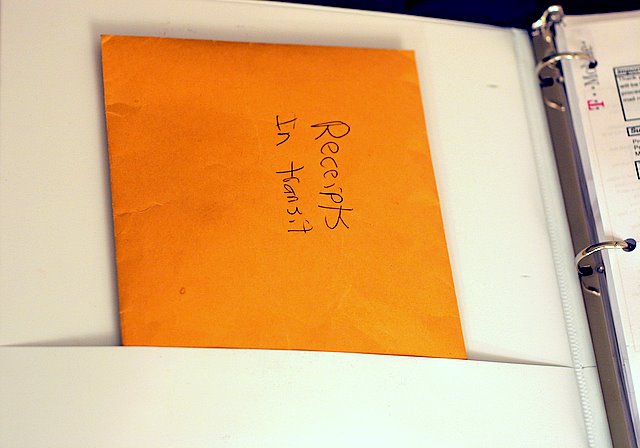

The only tools my method requires is a 3-ring binder, a hole puncher, and a stapler. Whenever I use my credit card or withdraw money from the ATM I keep the receipt so I can archive it later. First, they collect in my wallet and after a while the extra bulge becomes a real pain in my butt (literally). Their next holding bin is a small, manila envelope which I call receipts in transit.

This envelope sits in the pocket of my finance binder until the relevant statement comes in the mail. I punch holes in the statement so it can fit snuggly in my white binder and at the same time I go through the receipts in transit, picking out the relevant receipts. Comparing the amounts on the receipts to the amounts on the statement isn’t a bad idea. It is important to double check what your bank or credit card company is telling you since any mistake on their end can cost you money. Besides there is no law stating financial institutions are always right.

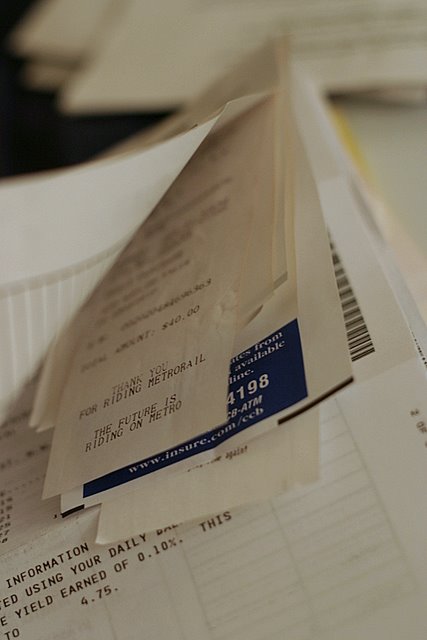

Next I staple the receipts to the statement so they will never be lost or misplaced. Now if for whatever reason I need to dig up a past receipt I can easily flip to the right statement and search through a handful of receipts instead of a whole shoe box full.

Once in my binder, the statements are filed in reverse chronological order or the latest statement is the first page I see. Most bills and bank statements get filed together including credit card bills, my cell phone bill, the cable bill, and my bank statements, all based on their closing date.

The hardest, and probably most important part, of making a system like this work is to keep up with it and organize your statements right when they come in. A little work every week can save a lot of headaches and hassle at the end of the year come tax time.

The New York Times has an ‘interactive graphic‘ to help you figure out where you stand in regards to the rest of the population when it comes to your socio-economic status.

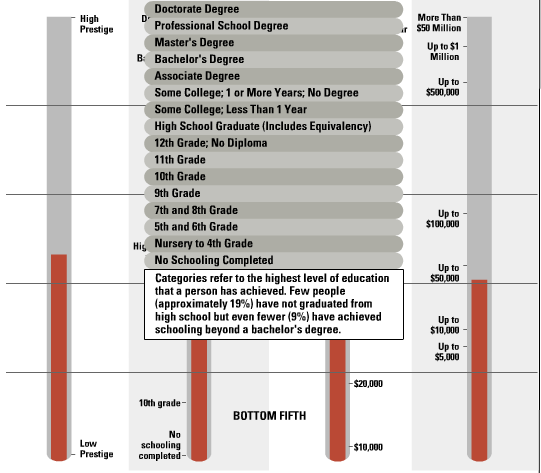

The interactive graphic allows you to enter information about your financial status, and then it displays a graph indicating where these factors place you on the socio-economic scale.

I find it astounding that if you have a undergraduate degree you are in the 91st percentile! In other words, only 9% of the population has a higher degree than you.

For the past month I have been tracking my weight with help from SkinnyR. Ever since my 22nd birthday I have been unhappy with how round my tummy has been and immediately set out to get my weight under control. I realize that I am now at a point in my life where I simply can’t eat anything I want and my lack of exercise isn’t helping my situation. I have been playing Wii Sports a little bit which has gotten my butt off the couch but I needed something else to help me get a good cardio workout in.

That is why I picked up this lovely beast…

The Voit Pro Series 5000! Now I can keep active while watching some TV. I hope to do 15-25 minutes a night and the best part is this exercise bike only cost me $7.42!

Thrift stores can be the source of some good deals and because today was Memorial Day, Value Village marked everything 50% off. The bike was originally $14.14, a modest deal if you ask me. But at the counter to my surprise the bike came out to $7.42 after tax. Now I won’t feel that bad if I decide an exercise bike isn’t right for me or if this exercise bike is really doing the trick I might step up and put down the money for a good quality bike. I’m hoping for the latter but we will just wait and see what happens.

How did I think to go to the thrift store? Simple. Six months ago I was trying to get rid of an old strength training machine and thought it would be good to give away to Good Will. I drove up to the donation lot and they refused to take it because they already had too much exercise equipment. Makes sense to me since a lot of people buy a crap-load of new fangled devices they see on TV only to rapidly lose interest after starting.

P .S. They also had an Ab Doer Extreme (pictured below) that looked brand new. I didn’t see the price but I guarantee you it was less than $80 that it is going for online. You just never know what you might find at a second hand shop.